EV Dashboard is Back

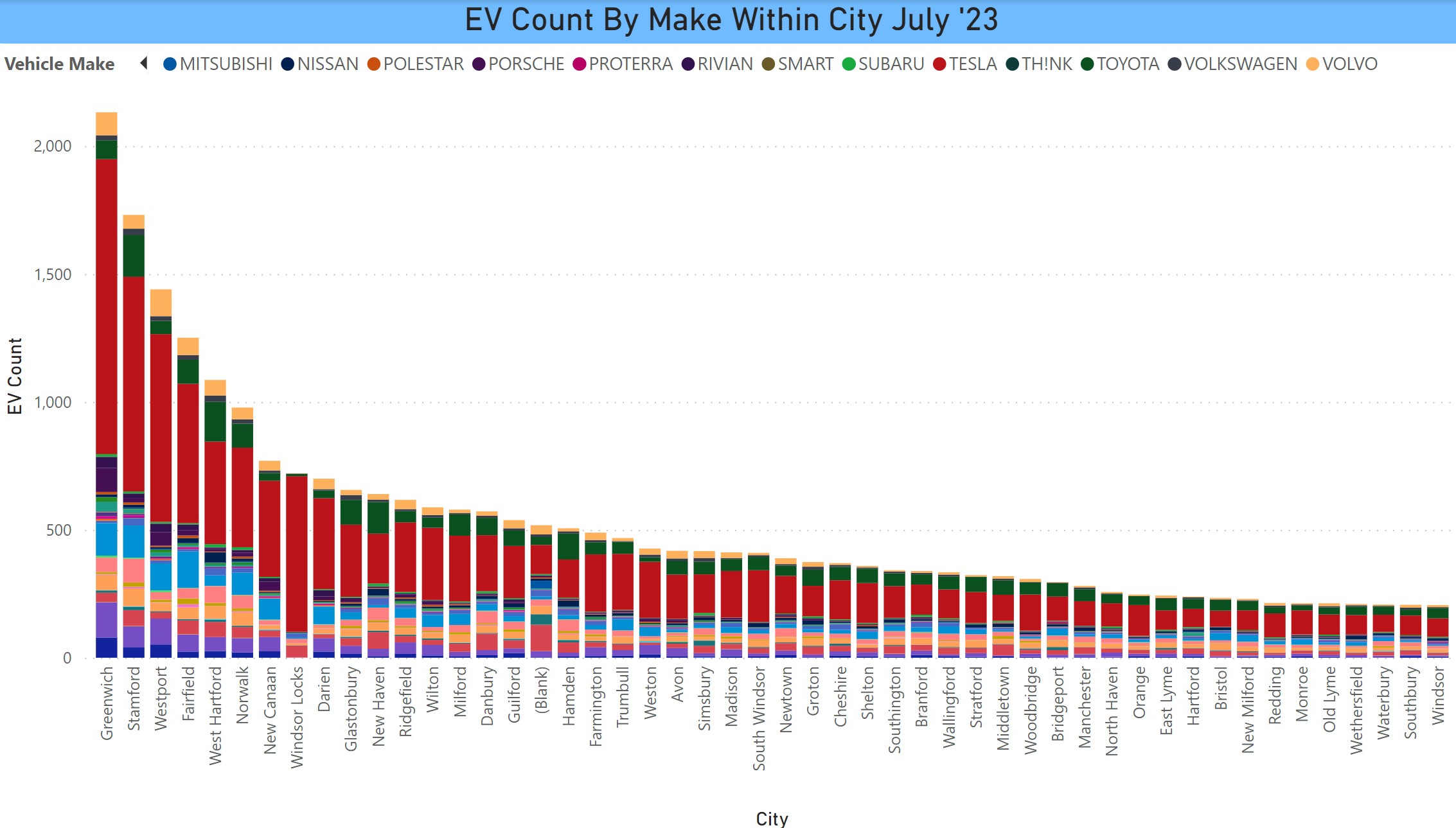

July 2023 Dashboard With Full Interactivity Link to the dashboard. We have published a new dashboard of all EVs registered in CT, updated for the data released as of July 1, 2023. The dashboard has … Read more

July 2023 Dashboard With Full Interactivity Link to the dashboard. We have published a new dashboard of all EVs registered in CT, updated for the data released as of July 1, 2023. The dashboard has … Read more

Photo at top taken under one of the solar canopies at the Hotel Marcel with the building in the background, from left to right: Daphne Dixon – Live Green CT, Paul Wessel – Greater New … Read more

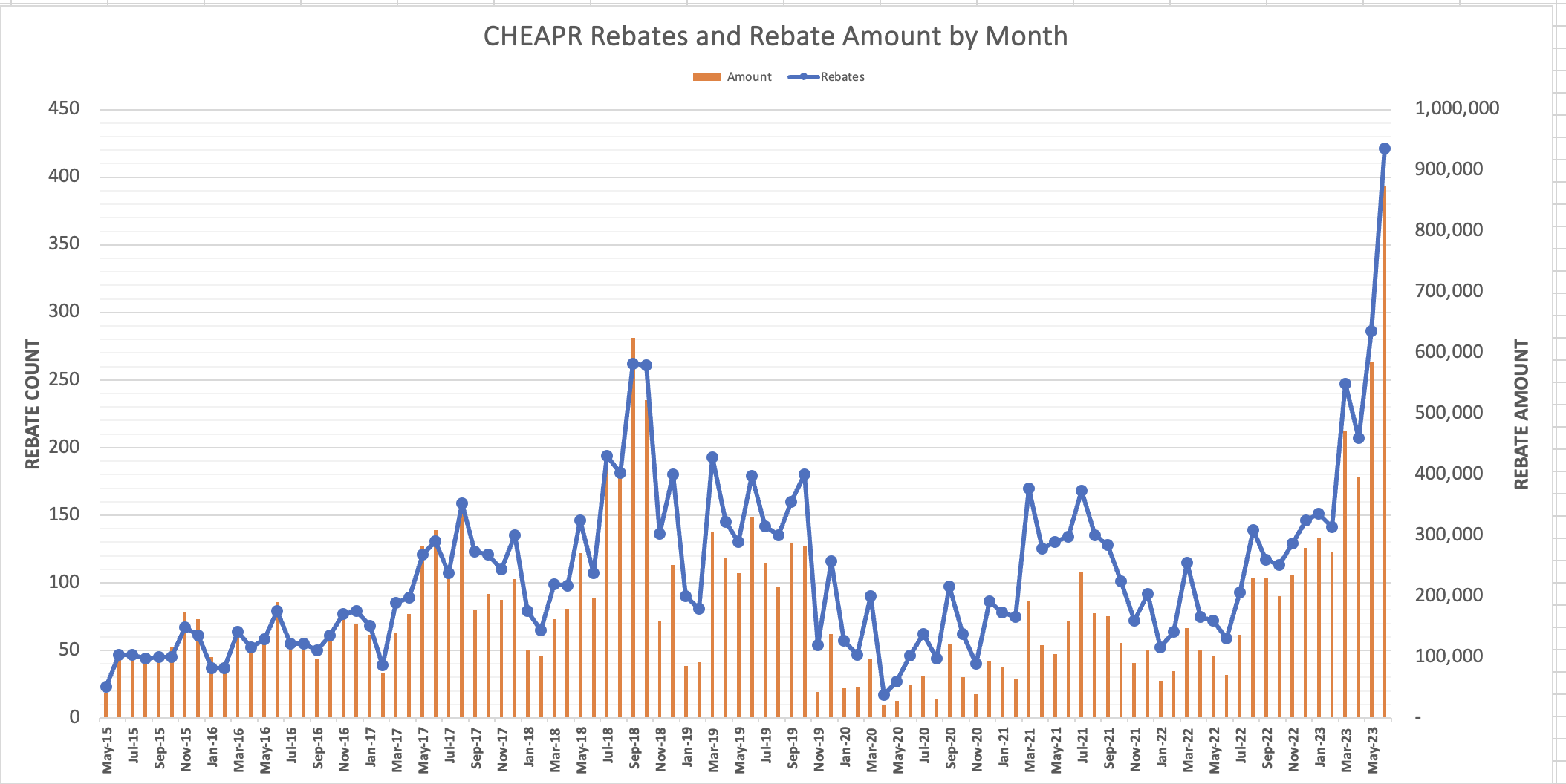

Tesla Model Y Leads Rebated Vehicles CHEAPR set another record in June in terms of rebates awarded with 421 rebates, way exceeding the previous high water mark that occurred just one month prior of 286. … Read more

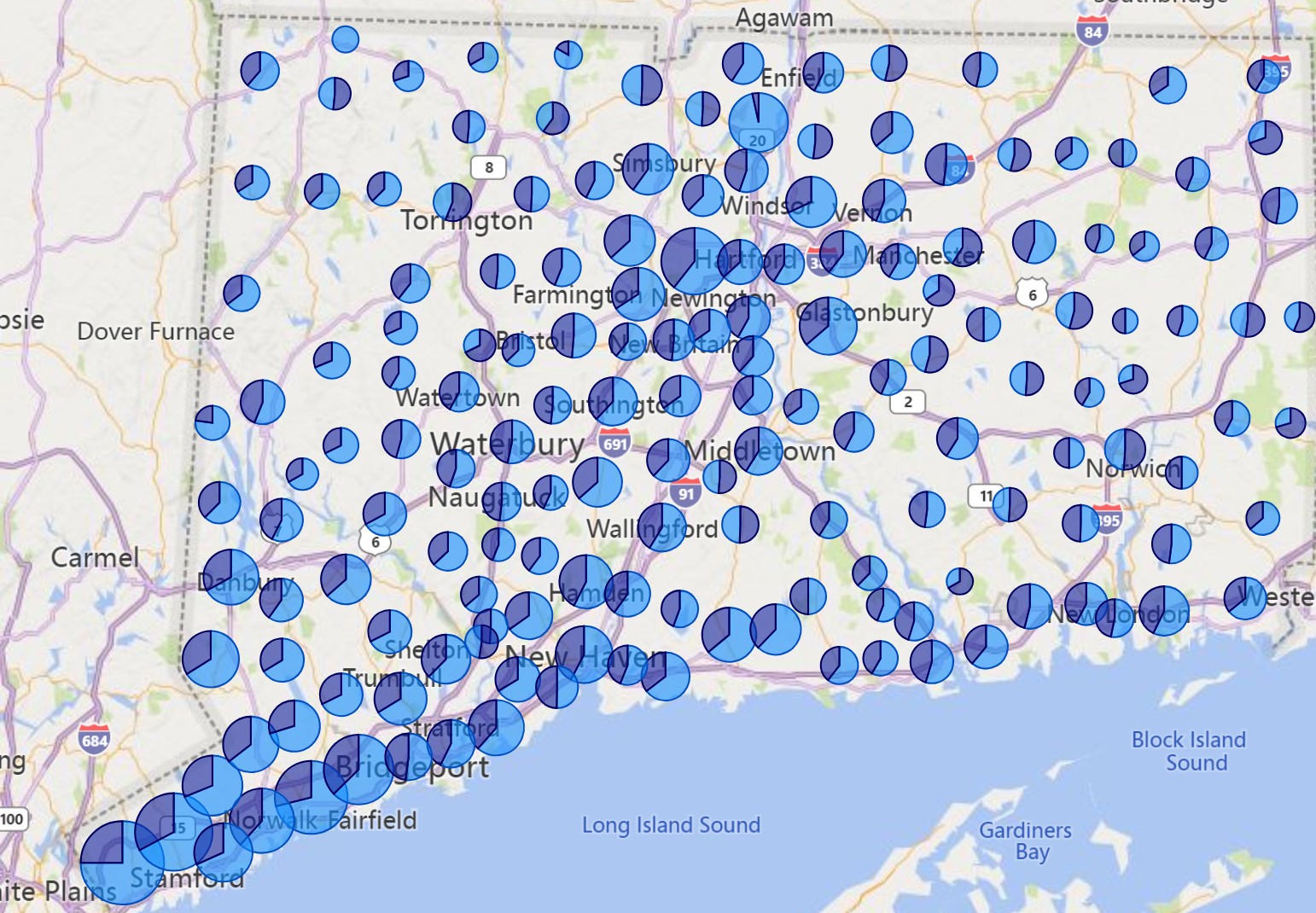

EVs by City and County Notes – There are differences every time we receive a file. In this case, the data do not include electric motorcycles and the handful of fuel-cell vehicles, which is different … Read more

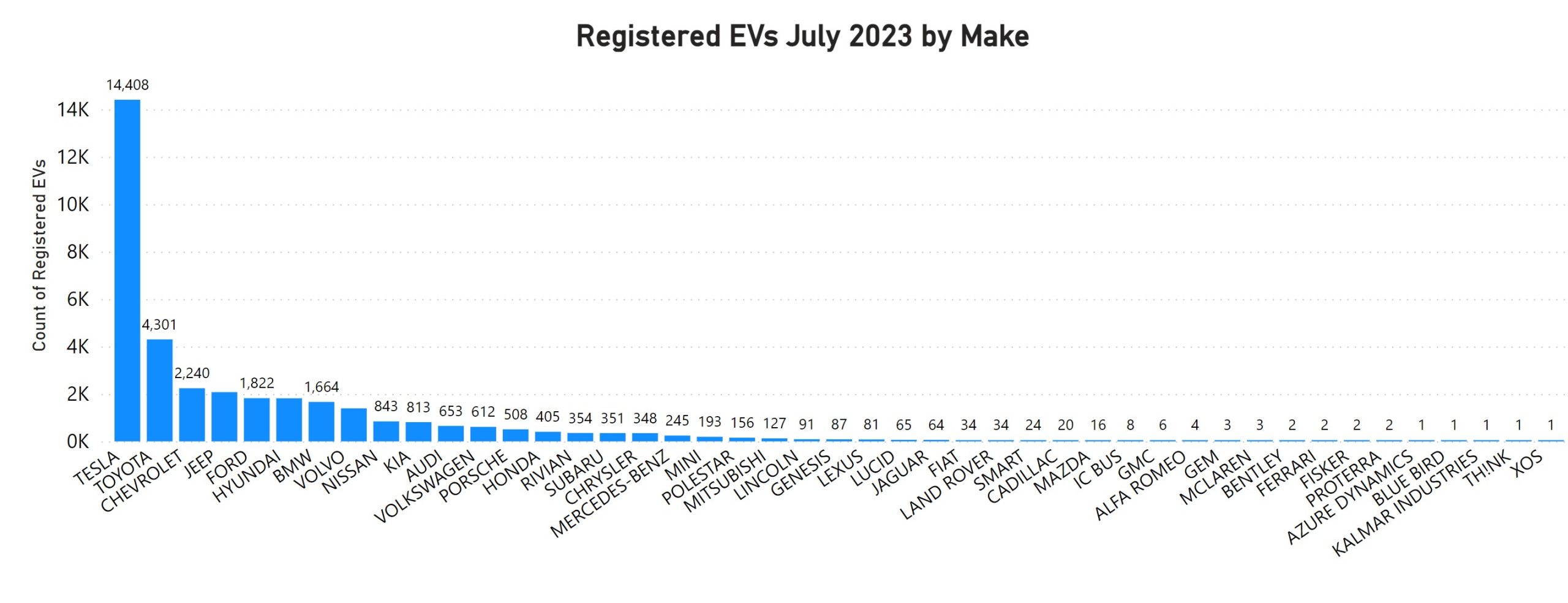

CT Hits 36K Registered EVs As Of July 1 We have not yet received a file from the DMV in response to our Freedom of Information Act Request. This information is pulled off the public … Read more

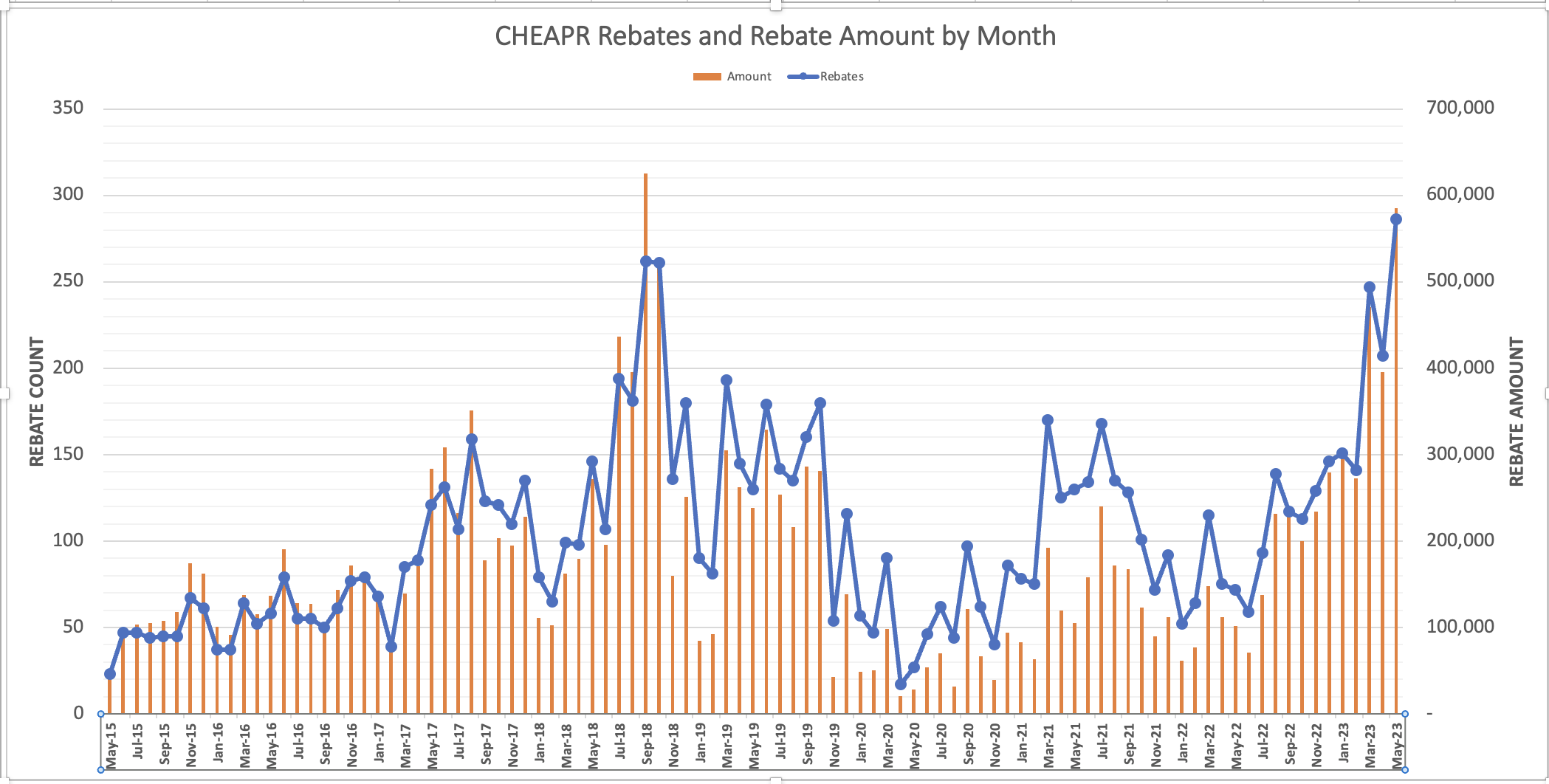

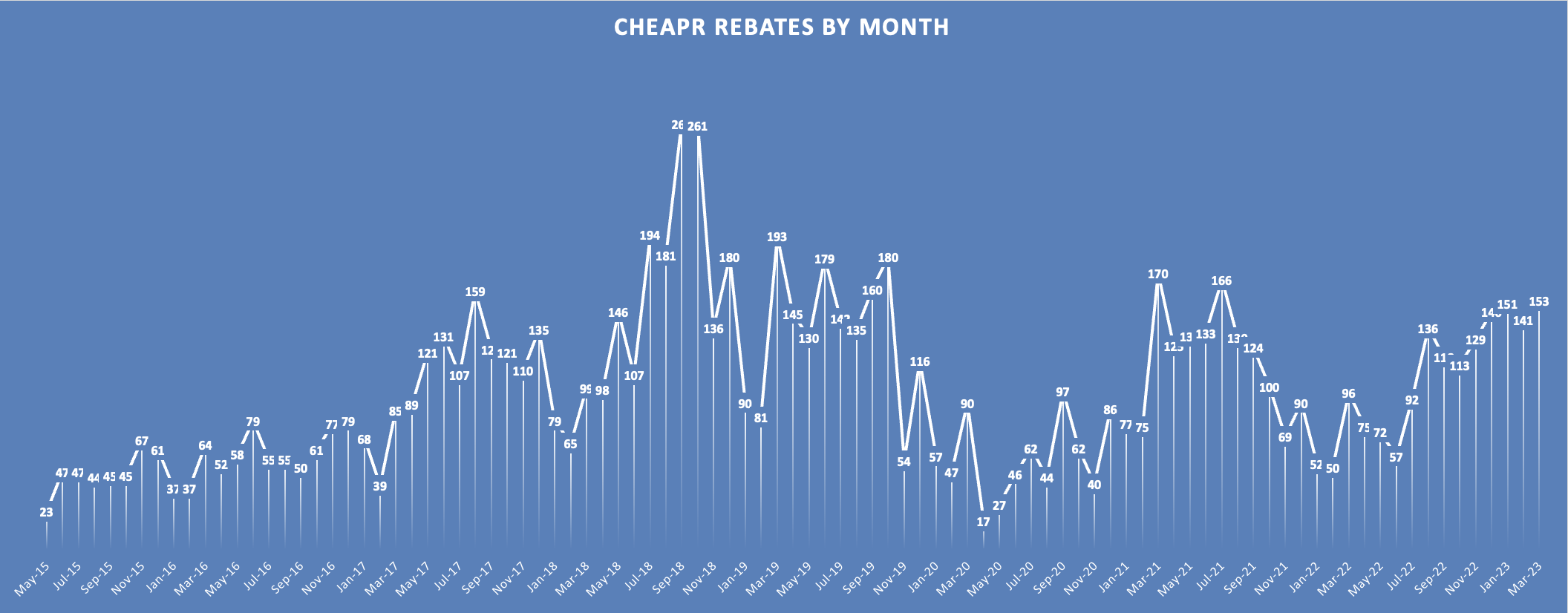

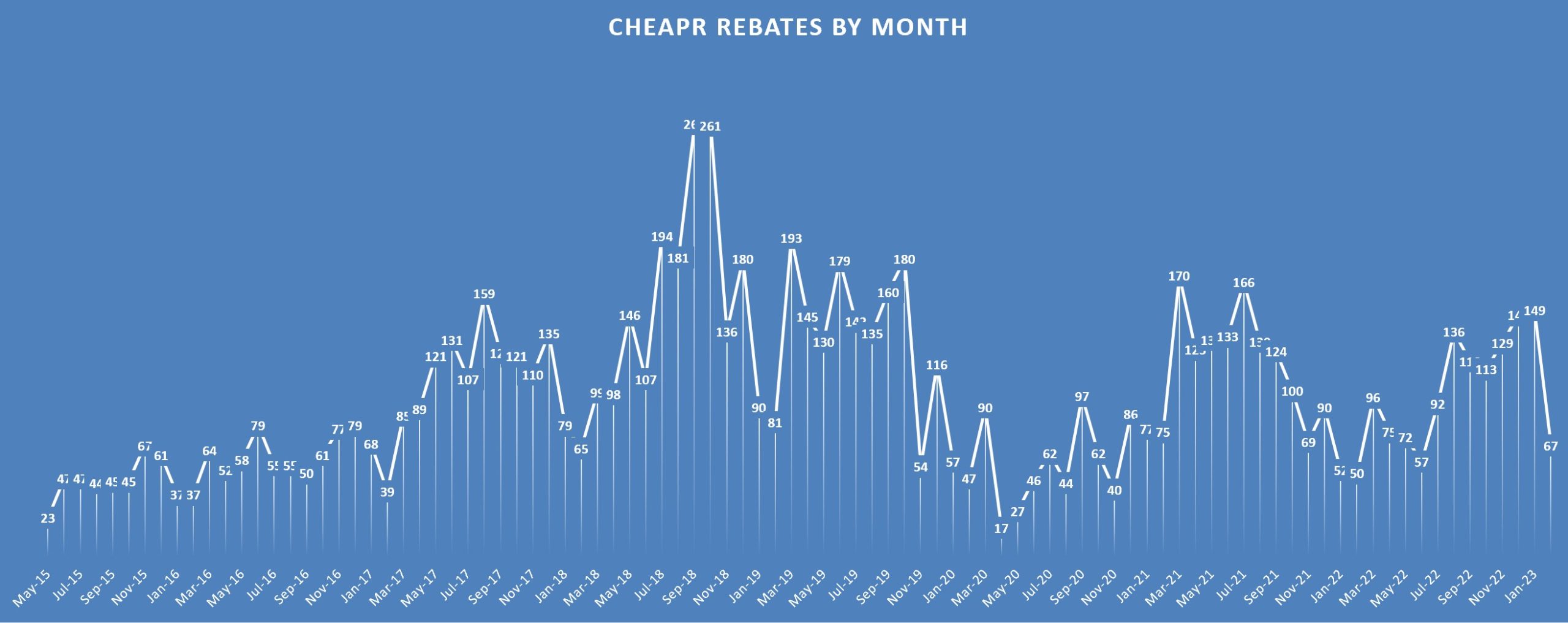

Rebates Way Up, Mostly Due to Tesla DEEP has published stats through June 14th, but for the purposes of this post, we are looking at complete months, thus through May 31st. As can be seen … Read more

Post by Barry Kresch Tesla Patrol Car Purchase Price Now Lower Than Ford Explorer ICE Police Vehicle In 2019, when the Westport Police purchased a Model 3 for use as a patrol car for $52,000 … Read more

Increase in Rebates Driven by Tesla Since the MSRP cap was increased in July 2022, there has been an increase in rebates as more models have become available. Somewhat predictably, it is driven mostly by … Read more

Updates on CHEAPR Implementation Almost one year ago, SB-4 was voted into law as Public Act 22-25, an environmental omnibus that made extensive changes to CHEAPR, the state EV purchase incentive program. The easiest change, … Read more

Post by Barry Kresch CHEAPR as a Proxy for EV-Friendly Dealers It is not unusual for a consumer to reach out to us, usually after a bad sales experience, and ask if we can recommend … Read more