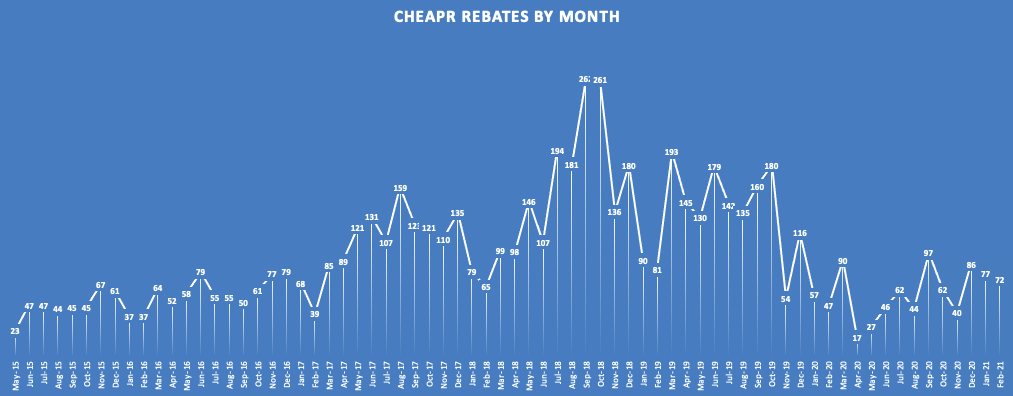

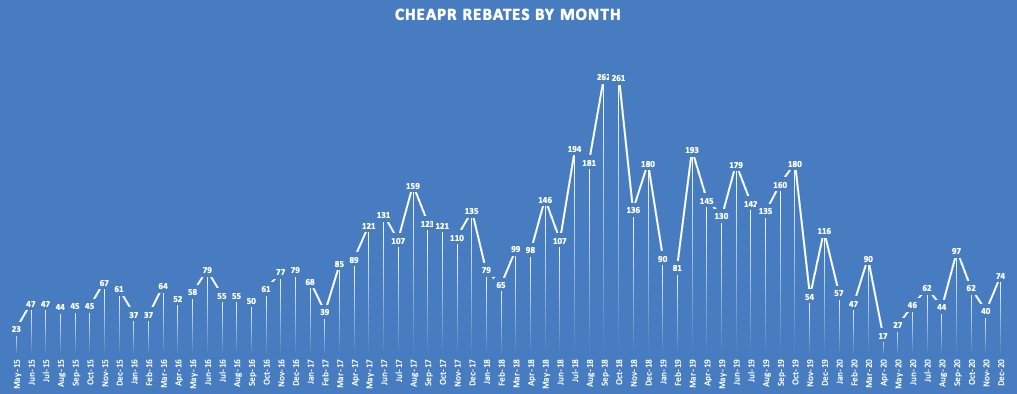

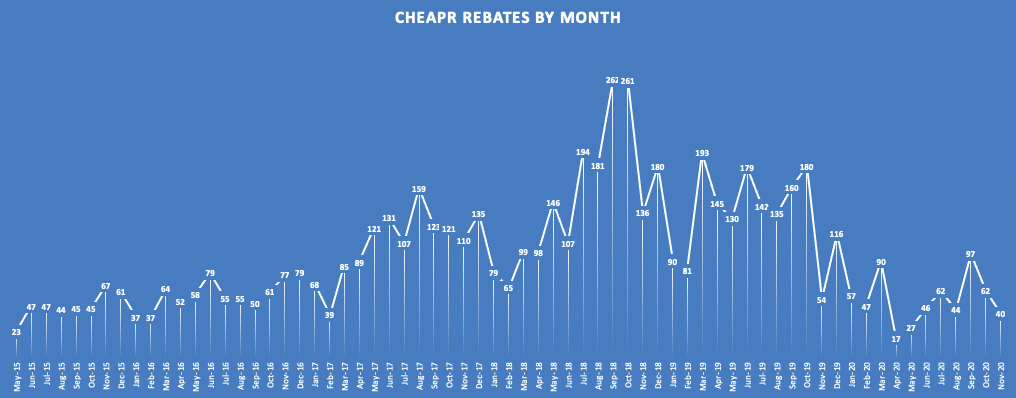

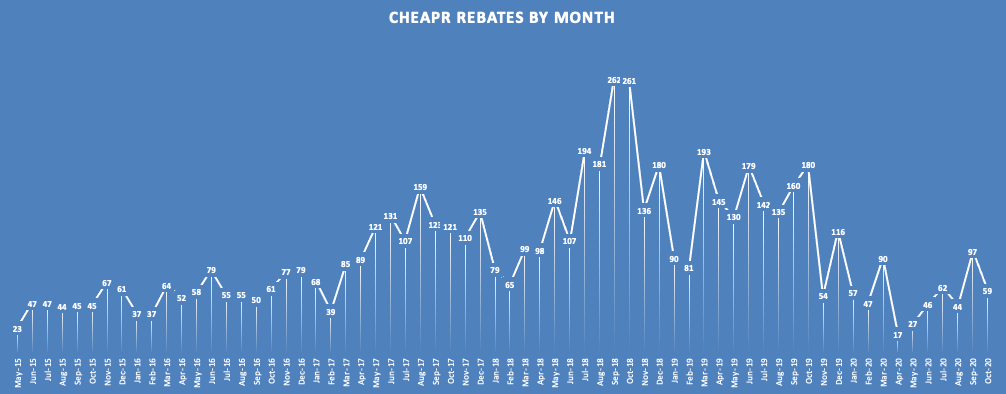

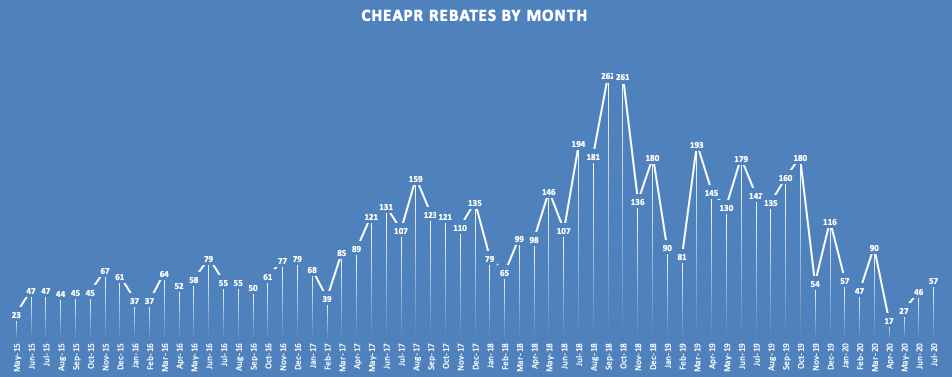

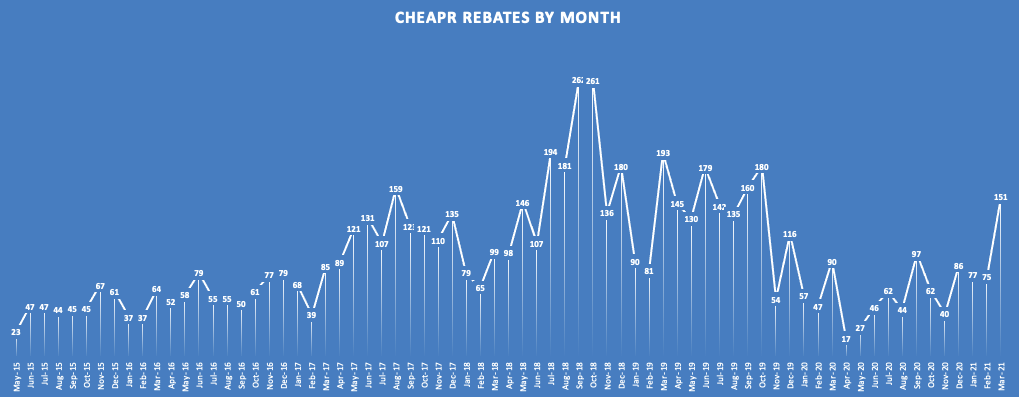

CHEAPR Rebates Up in March – Still No Word on Timing of Program Changes

Rebates Spike in March, but Program Still Underspent Rebates awarded under the state EV purchase-incentive program spiked to 151 in March, double that of the (slightly restated) number of 75 for February. This was part … Read more